The rapid advancement of artificial intelligence (AI) technologies has ushered in a new era of computing, bringing with it unprecedented demands on our digital infrastructure and energy resources. The escalating adoption of AI applications — from machine learning to large language models (LLMs) — has intensified the demand for substantial, large-scale computational resources.

Data centers are essential building blocks in the infrastructure supporting AI-driven applications. Meeting the needs of the AI revolution will hinge on not only building more data centers but also finding sustainable ways to power them. The relationships among data centers, AI-powered industries and the energy market — along with the role of technology and potential regulations — are at the heart of shaping this dynamic landscape.

What does the future hold for data centers? Answering that question requires a deeper understanding of the power sources that will fuel their growth.

With AI technology accelerating at an unprecedented pace, the market for data centers is undergoing an exponential shift. Hyperscalers — companies that operate massive data center infrastructure to support AI and cloud services — are at the forefront of this transformation.

AI workloads generally require higher power densities than traditional cloud computing. However, the industry is rapidly adapting to these new demands. While purpose-built AI infrastructure is still in its early stages, many existing data centers are being upgraded to accommodate AI workloads.

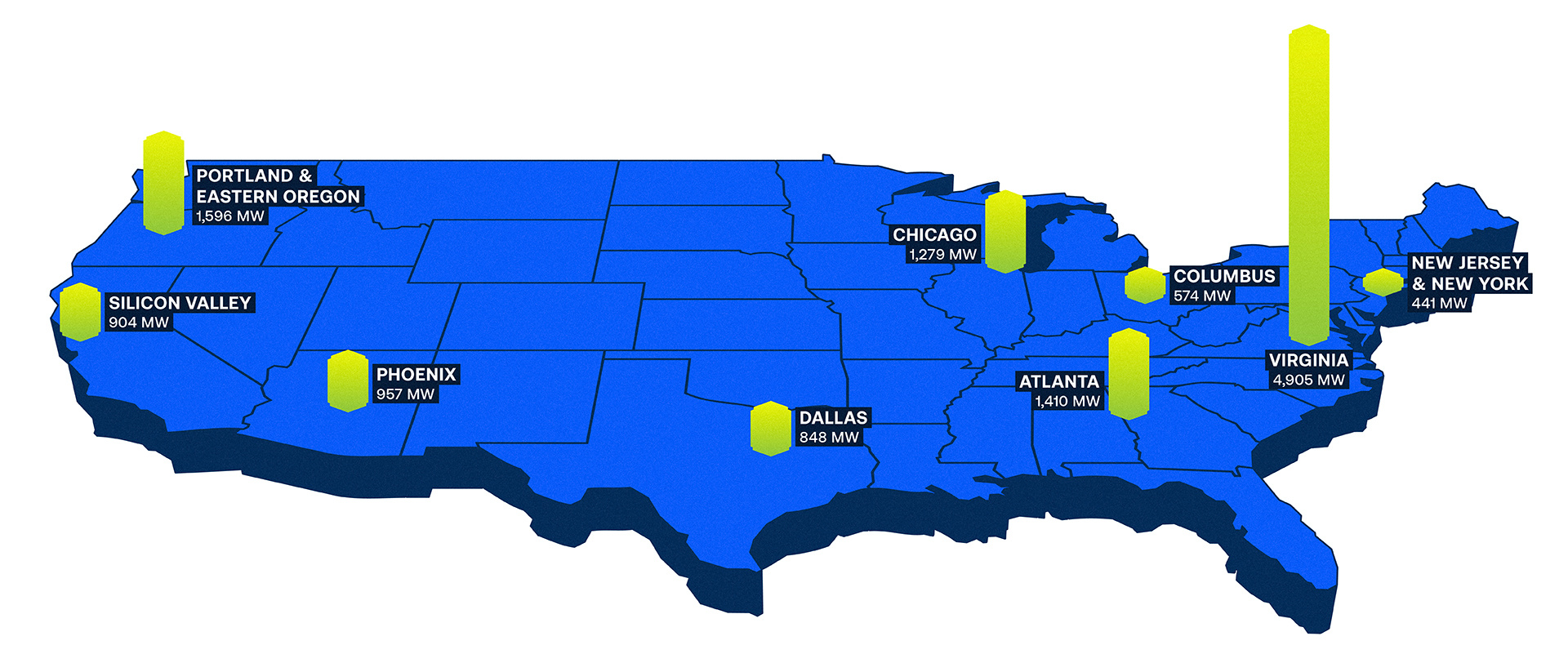

The power consumption demands of AI-focused data centers are enormous, and the amount of available energy varies greatly, depending on location.

Data centers have undergone a remarkable transformation in power consumption over the past 15 years, says Christine Wood, a vice president at Burns & McDonnell and leader of the mission-critical market sector. In the past, a 12-megawatt (MW) data center was considered substantial. Today, hyperscale data center campuses commonly range from 60 MW to several hundred megawatts. However, the rise of AI has accelerated this trend, pushing power requirements even higher.

For contrast, the city of Dallas, Texas, has peak demand of 3 gigawatts (GW) to 5 GW for the entire city. And the Dallas area is among the largest growth markets in the U.S. for data centers.

These data centers are a big challenge in both power generation and electric infrastructure. The shift to AI-specific facilities spotlights the need for scalability and sustainable design.

U.S. data center electricity demand is expected to reach 35 GW in the next five years, according to Utility Dive. As demand grows, teams are under increasing pressure to design for higher power densitties while keeping consumption efficient and sustainable.

This begs an obvious question: Can the energy sector keep pace with the growing needs of AI? Wood says the answer is yes, but it’s complicated.

While requests are rapidly escalating to assess power availability for new data center sites, their development presents unique challenges. The costs involved are substantial, requiring not only significant capital investment but also specialized experience in areas like on-site substation construction and strategic power agreements.

Power generation and storage solutions will be key to sustaining the growth of AI data centers. Recent integrated resource plans (IRPs) indicate that utilities are planning for the largest increase in gas plants in over a decade to address immediate needs, with dramatic increases in renewable energy usage expected over the course of the next 5 years to balance and maintain grid reliability.

Chris Ruckman, a vice president at Burns & McDonnell focused on energy storage, emphasizes the role of storage systems in managing fluctuating demand.

“Energy storage systems are becoming critical for managing peak loads and maintaining resilience,” Ruckman says. “Data centers will increasingly rely on these systems to avoid overburdening the grid.”

Some regions of the U.S. are feeling the strain of AI data centers more acutely than others. Power availability is a major concern for the industry, particularly in high-demand areas like Northern Virginia near Washington, D.C.

“With its concentration of hyperscale data centers, Northern Virginia is pushing the limits of power capacity,” Ruckman says. “Over 70% of global internet traffic already flows through the region, and the power demand for data centers in the area has increased by about 500% over the last decade.”

The data center capacity in Northern Virginia alone surpasses every other individual country outside the U.S. except China. Other major data center markets in the U.S. include Dallas, Texas; Phoenix, Arizona; Columbus, Ohio; and several cities across the Midwest.

.svg)

.svg)

.svg)